In the world of corporate finance, stock options are a common form of employee compensation. However, accounting for these options can be complex, especially under the United States Generally Accepted Accounting Principles (US GAAP). This article delves into the intricacies of US GAAP accounting for stock options, providing a comprehensive guide for both finance professionals and individuals interested in this topic.

What are Stock Options?

Stock options are contracts that give employees the right to purchase a specific number of company shares at a predetermined price within a specified period. These options are typically granted to employees as part of their compensation package, serving as an incentive to boost their performance and align their interests with those of the company.

The Challenges of Accounting for Stock Options

Accounting for stock options under US GAAP can be challenging due to several factors:

- Complexity: The valuation of stock options requires complex calculations and assumptions, making it difficult for companies to determine the fair value of these options.

- Subjectivity: The valuation process involves subjective assumptions, which can lead to inconsistencies in reporting.

- Regulatory Compliance: Companies must comply with strict regulations when accounting for stock options, which can be time-consuming and resource-intensive.

Key Aspects of US GAAP Accounting for Stock Options

To account for stock options under US GAAP, companies must follow several key steps:

- Determine the Grant Date: The grant date is the date on which the stock options are granted to employees. This date is crucial for calculating the fair value of the options.

- Estimate the Expected Life: The expected life is the period over which the employee is expected to hold the stock options. This estimate is based on factors such as employee turnover and the vesting period.

- Determine the Volatility: The volatility of the company's stock is a key factor in determining the fair value of the options. This can be challenging, as it requires analyzing market data and making assumptions about future stock price movements.

- Calculate the Fair Value: Once the expected life and volatility are determined, the fair value of the stock options can be calculated using a valuation model, such as the Black-Scholes model.

- Recognize the Expense: The fair value of the stock options is recognized as an expense over the vesting period. This expense is typically recorded in the income statement and can significantly impact a company's financial performance.

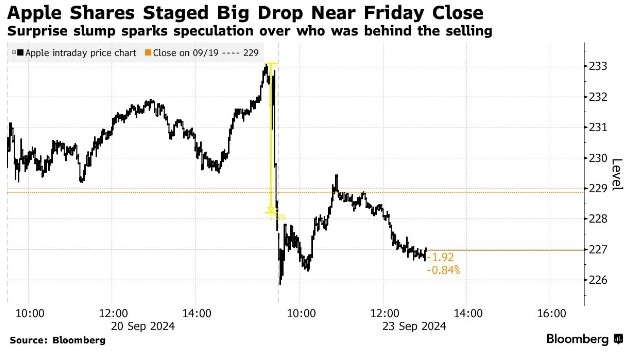

Case Study: Apple Inc.

To illustrate the application of US GAAP accounting for stock options, let's consider a case study of Apple Inc. In its fiscal year 2020, Apple granted approximately 10 million stock options to employees. The fair value of these options was determined to be

Conclusion

Understanding US GAAP accounting for stock options is crucial for finance professionals and individuals interested in corporate finance. By following the key steps outlined in this article, companies can ensure accurate and compliant reporting of stock option expenses. As the landscape of corporate finance continues to evolve, staying informed about these accounting principles is essential for making informed decisions.

vanguard total stock market et