In the world of finance, stock-based compensation is a crucial aspect for companies, especially those listed on U.S. stock exchanges. This form of compensation is governed by the U.S. Generally Accepted Accounting Principles (GAAP). This article delves into the nuances of stock-based compensation under US GAAP, providing a comprehensive understanding of its implications and importance.

What is Stock-Based Compensation?

Stock-based compensation refers to the granting of equity instruments to employees or directors in exchange for services rendered. These equity instruments can be stocks, stock options, restricted stock units (RSUs), or other forms of equity awards. The purpose of stock-based compensation is to align the interests of employees with those of the company, potentially leading to increased productivity and performance.

Why is Stock-Based Compensation Important?

Stock-based compensation is a vital tool for attracting and retaining talent, especially in industries where competitive salaries are not feasible. It provides employees with a stake in the company’s success, encouraging them to work harder and contribute more effectively. Moreover, it helps companies to manage their expenses, as stock-based compensation is typically tax-deductible for employers.

US GAAP and Stock-Based Compensation

Under US GAAP, stock-based compensation is accounted for using the fair value method. This method requires companies to estimate the fair value of the equity instruments granted and recognize the expense over the employee’s service period. Here’s a breakdown of the key aspects:

1. Valuation of Equity Instruments

The fair value of equity instruments is determined using various models, such as the Black-Scholes model for stock options and the binomial model for RSUs. The valuation process involves considering factors like the expected volatility of the company’s stock, the expected term of the award, and the risk-free interest rate.

2. Expense Recognition

Once the fair value is determined, the expense is recognized over the employee’s service period. This means that the expense is recognized ratably over the vesting period of the award. For example, if an employee is granted 1,000 RSUs with a vesting period of four years, the expense will be recognized at a rate of 250 RSUs per year.

3. Disclosure Requirements

Companies are required to disclose detailed information about their stock-based compensation plans, including the valuation methods used, the expense recognized, and the impact on financial statements. This information helps investors and stakeholders to understand the potential risks and rewards associated with stock-based compensation.

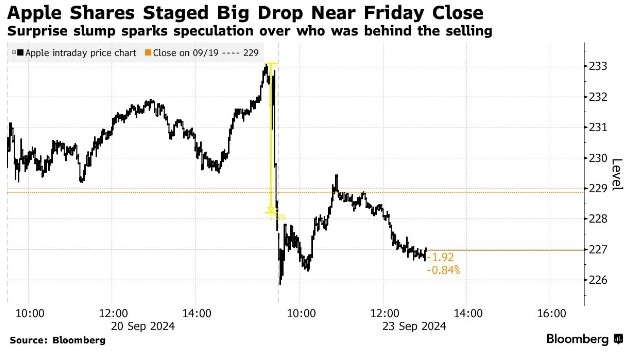

Case Study: Apple Inc.

To illustrate the application of US GAAP in stock-based compensation, let’s consider the case of Apple Inc. In its fiscal year 2020, Apple granted approximately 15 million restricted stock units (RSUs) to employees. The fair value of these RSUs was determined to be

Conclusion

Understanding stock-based compensation under US GAAP is essential for companies and investors alike. By following the fair value method and recognizing expenses over the service period, companies can effectively manage their compensation costs while aligning the interests of employees with those of the company. As the landscape of corporate finance continues to evolve, staying informed about stock-based compensation is more important than ever.

vanguard total stock market et